Last Updated on May 25, 2026

Financial data quality management is the set of processes, ownership structures, and controls that finance and IT teams use to ensure transactional, reference, and master data stays accurate, complete, and consistent across systems. It covers everything from how vendor records are standardized in an ERP to how customer identities are resolved across a payments platform and a core banking system. The discipline sits at the intersection of data governance and financial operations, and in regulated industries, it carries direct compliance weight.

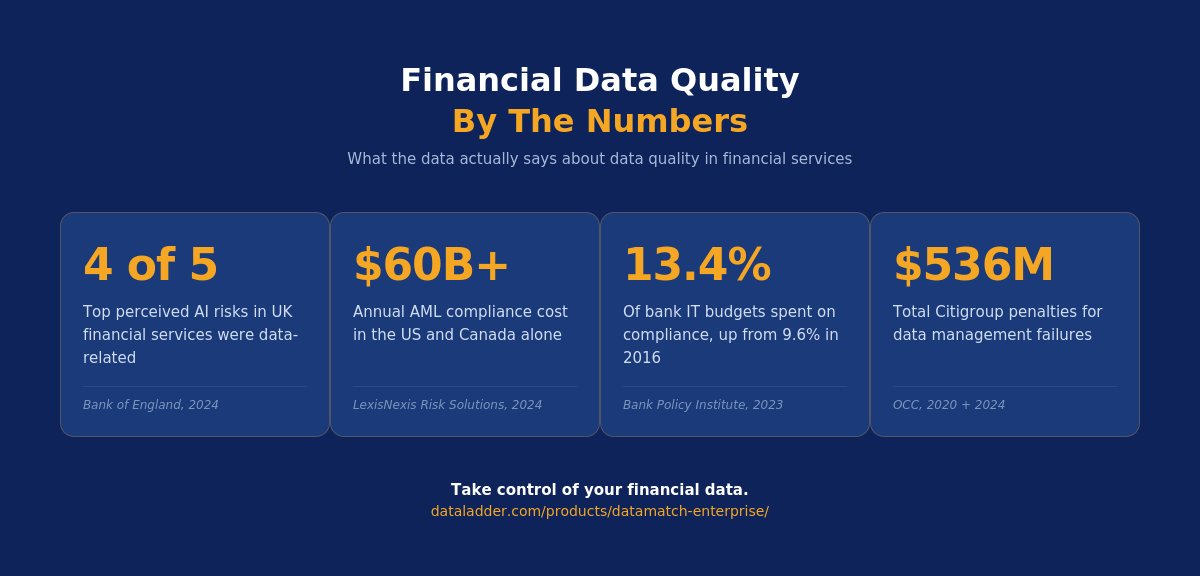

According to a 2024 Gartner report, 64% of financial decisions are now powered by data, yet only 9% of finance professionals fully trust the financial data they rely on. That gap doesn’t close on its own. It widens every time a new system comes online, a merger adds an unreconciled data source, or a regulatory mandate requires reporting that the current data architecture wasn’t built to support.

The costs of bad financial data don’t concentrate in one place either. There’s no single line item labeled “bad data expense” on a P&L. Instead, the cost surfaces as delayed closes, failed reconciliations, rejected payment files, and compliance remediation that each look like isolated incidents.

Consider that your quarterly close is three days late because the same vendor appears in SAP as “Accenture LLP,” in the legacy AR system as “Accenture PLC,” and in the payments platform as “Accenture Plc.” Three different kinds of records exist for one entity but there’s no consensus on which carries the correct banking details. Cases like these are not one-off hypothetical scenarios. This is the reality of what happens when financial data quality management is not built into how systems and teams operate.

To put things in perspective, Citi was fined $400 million in 2020 for inadequate data governance and internal controls, then hit with an additional $136 million in 2024 for failing to make sufficient progress on regulatory reporting. Even though those penalties were years apart, the underlying cause was that data management failures were not resolved even in all those years.

This guide is for the finance and IT teams responsible for building something better.

What Is Financial Data Quality Management?

Financial data quality management is the discipline of ensuring that the data flowing through financial systems is accurate, complete, and consistent enough to be relied on for reporting, risk management, and regulatory compliance. It spans the full lifecycle of financial data from how it enters a system to how it’s validated, standardized, and maintained over time.

In financial services, data governance defines the standards such as what a valid customer record looks like, which system is the source of truth for counterparty data, and who has authority to make changes.

Data quality management is the operational work of meeting those standards, profiling, validating, cleansing, and monitoring the actual data against the rules governance put in place.

TABLE 1 — DATA QUALITY DIMENSIONS MAPPED TO FINANCIAL WORKFLOWS

| DQ Dimension | Finance Workflow | Failure Example | Downstream Impact |

|---|---|---|---|

| Accuracy | GL reconciliation | Wrong cost center mapping on entity name | Trial balance does not tie; close delayed |

| Completeness | KYC / onboarding | Missing beneficial owner on corporate account | AML screening gap; regulatory finding |

| Consistency | Cross-system customer ID | Same client has three IDs across CRM, core banking, and trade | Exposure calculation breaks; fragmented customer view |

| Timeliness | Intraday liquidity | Balance feed arrives 90 minutes late | Liquidity position misstated; limit breach risk |

| Uniqueness | Counterparty master | Duplicate LEI records for same entity in two business lines | Double-counted exposure; duplicate payments |

| Validity | SWIFT BIC / IBAN / LEI | Malformed BIC passes internal validation, fails SWIFT routing | Payment rejected at settlement |

What Does Poor Financial Data Quality Actually Cost?

The question isn’t whether poor data quality is expensive. For financial institutions operating across multiple systems, regulatory frameworks, and business units, the real question is how much of that cost is actually visible to the people accountable for it.

Most of it isn’t. Compliance, finance, and IT each absorb a piece of the damage in their own domain, which means nobody is looking at the full picture. Without that, the problem stays underfunded and under-prioritized until something forces the issue.

Costs split into three buckets: operational, regulatory, and strategic. Most organizations only track the first one, which is why the full figure surprises leadership when someone finally puts it together.

Reconciliation is the most visible operational cost. When subledger records do not match the GL, finance teams resolve exceptions manually. In a large institution, that is hundreds of analyst hours per close cycle.

Duplicate vendor records add another layer of complexity as a team processing thousands of invoices against a dirty vendor master will periodically pay the same invoice twice, and not all overpayments get recovered.

Regulatory costs are categorically different because they do not scale with volume. A single enforcement action can wipe out years of operational savings. AML fines globally increased by 417% in H1 2025 year-over-year, totaling approximately $1.23 billion, with sanctions screening failures and inadequate customer due diligence, both data quality failures, driving the largest penalties.

The cost calculation most teams never run is straightforward once you have the inputs. Multiply weekly reconciliation hours by fully-loaded FTE cost, annualize it, then add regulatory remediation, duplicate payment losses, and delayed-decision opportunity cost. Even if you run it with conservative inputs, the number will still be larger than leadership expects.

A Five-Step Financial Data Quality Framework

Data quality initiatives in financial institutions need to be implemented with extra care due to financial risks. A working framework has five steps: profile what you have, define DQ rules tied to financial outcomes, cleanse and standardize, apply data matching and entity resolution, then monitor continuously. Both finance and IT own pieces of every step.

Financial services organizations operate under a level of scrutiny that makes current data quality a baseline requirement, not an aspiration. Regulatory bodies expect accurate and complete data across financial reporting, customer data, and risk management functions. When data integrity breaks down, whether through inconsistent data entry, missing data, or fragmented records across systems, the downstream consequences hit compliance, credit risk models, and audit trails simultaneously.

Maintaining high data quality at scale in financial institutions requires more than good intentions and periodic cleanup. The organizations that maintain data quality consistently are the ones that have moved from reactive fixes to structured data management practices, supported by the right data quality tools and robust data governance frameworks. Without continuous monitoring and a systematic approach to improving data quality, even well-staffed data teams find themselves chasing problems that should never have reached production.

The framework below is built around that reality. Each step is designed to help financial institutions establish reliable financial data as a foundation, with data profiling and data monitoring tools playing a central role throughout.

Step 1: Profile Before You Fix

Profiling means systematically characterizing your data before trying to clean it. For financial data, that means null rates, format distributions, and uniqueness ratios across the fields that drive your workflows: counterparty legal entity names, customer IDs, account codes, currency codes, and reporting period dates. Data profiling tools handle this at scale, scanning across connected financial systems and surfacing cross-system consistency gaps in minutes rather than days.

What profiling actually reveals is where your data collection processes are introducing noise. Incomplete data at the point of entry, whether from manual data entry best practices not being followed or from upstream system mismatches, compounds fast in finance. A counterparty name entered inconsistently across three systems doesn’t just create a duplicate record; it distorts any downstream analysis that relies on that entity. When you profile across all data quality dimensions simultaneously, patterns emerge that point directly to the source of potential data quality issues rather than just their symptoms.

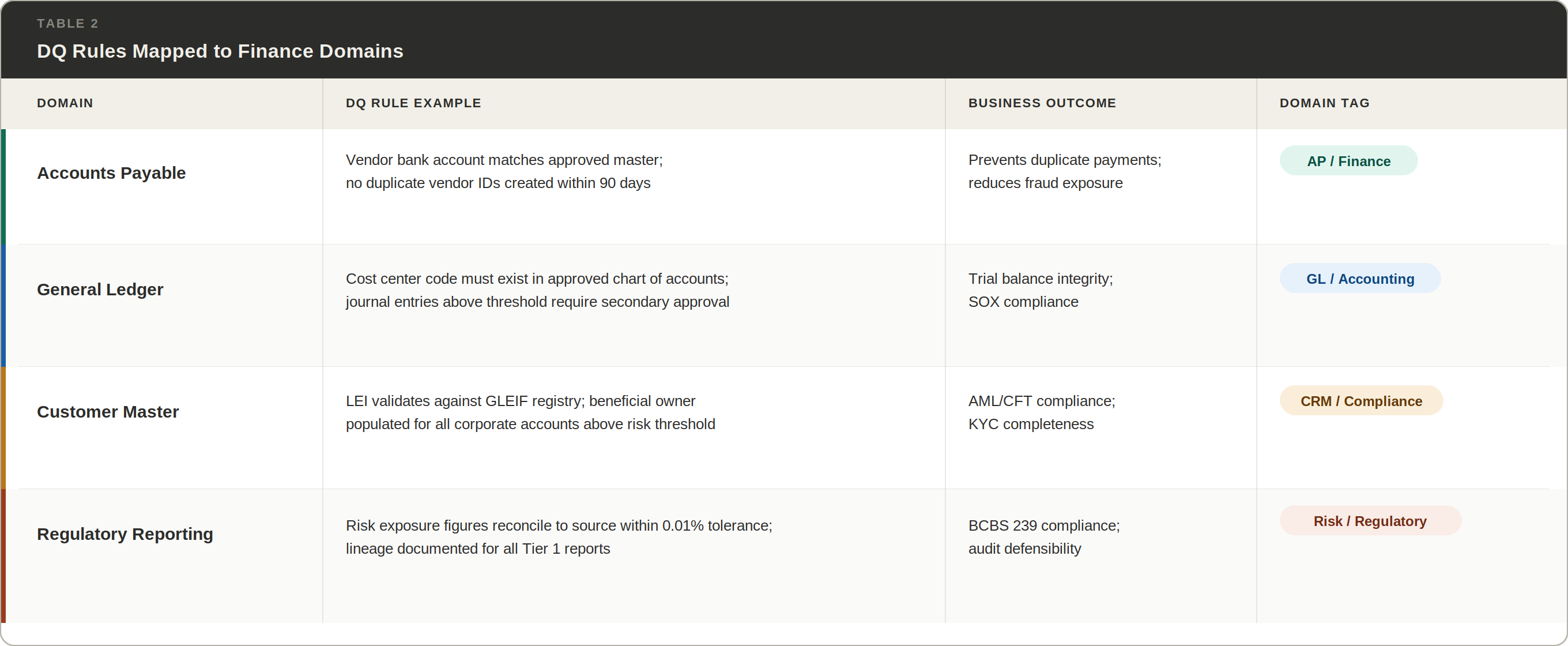

Step 2: Define Rules Against Business Outcomes

Rules like “field must not be null” catch technical errors but miss business-critical failures. Rules defined by finance teams against actual workflow requirements are categorically more useful. A vendor master rule should read: “Vendor bank account must match approved vendor master; no duplicate vendor IDs created within 90 days.” Not “VendorBankAccount IS NOT NULL.”

The financial industry has learned this the hard way. Validation rules written by IT in isolation from finance workflows produce quality data by technical standards while still generating incorrect financial statements. The key components of a rule set that actually works are specificity to the financial sector workflow it governs, ownership by the data stewards closest to that workflow, and tolerance thresholds calibrated to regulatory requirements. When you assign data stewards to each domain and give them accountability for rule definition, the rules stop being a compliance checkbox and start functioning as an enforcement layer that financial institutions rely on to protect both operations and audit trails.

Data validation rules tied to business outcomes also give you the ability to analyze trends in rule violations over time. When a rule fires repeatedly on the same field or source system, that is a signal worth investigating, not just a row to remediate. Teams that use data validation this way, with strict data governance around rule ownership and exception handling, are the ones using data cleansing tools to fix root causes rather than re-cleaning the same records quarter after quarter.

Step 3: Cleanse, Standardize, and Resolve Entities

Cleansing in finance means standardizing legal entity names to their authoritative form, normalizing address formats, converting currency codes to ISO 4217, and correcting malformed SWIFT BIC codes against the official registry. The harder problem is entity resolution, which is where most programs stall.

Deterministic matching fails when unique identifiers like LEIs or tax IDs are missing, incorrect, or formatted inconsistently across systems. Probabilistic and fuzzy matching scores potential matches across multiple fields simultaneously: legal entity name, registered address, country of incorporation, and any identifiers present. Records above a confidence threshold merge into a golden record. Records in a review band route to a human. Records below threshold stay separate.

Corporate hierarchy resolution adds another layer. Identifying that three subsidiary records belong to the same ultimate beneficial owner requires matching on organizational relationships, not just entity attributes. For AML screening and aggregate exposure calculation, missing that linkage is a material failure.

Ready to improve data matching in your environment?

DataMatch Enterprise has been independently benchmarked to find 5 to 12% more matches than IBM and SAS equivalents with fewer false positives.

Start a Free TrialStep 4: Monitor Continuously

A program that cleanses without monitoring is a one-time project. Monitoring means automated checks running at defined intervals, generating scores against your DQ rules, and routing exceptions to the right owners before they hit downstream systems. The output for finance leadership should be a scorecard tied to business metrics: match rate on counterparty records, exception volume by process, and days-to-remediate. A technical DQ score with no business translation will not survive a budget review.

Step 5: Govern What You’ve Built

Monitoring tells you when something is wrong. Governance determines what happens next, who owns it, and how you prevent the same failure from recurring. Without that structure, even a well-instrumented program degrades as personnel change, legacy systems get patched in ways that shift data formats, and new source feeds get added without going through any validation gate. Data quality goals need to be documented at the domain level, with named data stewards accountable for each one. When transaction data from a new source starts arriving with inconsistent formats, there should be a defined process for catching that at ingestion. When customer information or sensitive data is involved, that process also needs to intersect with data security and access controls, since quality failures in those fields carry regulatory weight beyond operational inconvenience.

A structured approach to governance also closes the handoff gap between finance and IT. Both teams own pieces of every step in this framework, but without clear escalation paths and documented rule ownership, timely data remediation stalls in review queues. The organizations that sustain high data quality over multiple years treat governance as operational infrastructure rather than a compliance deliverable. They assign data stewards with real authority, support compliance requirements through automated rule enforcement, and revisit data quality goals as business conditions change.

Where Regulatory Requirements Create Non-Negotiable DQ Standards

Data quality is not uniform in its regulatory consequences. Three workflows carry the most enforcement risk: risk data aggregation under BCBS 239, AML and sanctions screening, and core system migrations.

BCBS 239 requires globally systemically important banks to produce accurate, complete, and timely risk data on demand. The ECB’s 2024 RDARR Guide identified data taxonomy inconsistencies and inability to generate accurate consolidated views under stress as the most common compliance failures. Periodic penalty payments for non-compliance can reach 5% of average daily turnover per day, and the ECB has signaled these are now active enforcement tools, not theoretical ones.

AML and sanctions screening is only as good as the customer data behind it. Incomplete UBO information means sanctions checks miss beneficial owners of shell structures. Fragmented records create screening blind spots. The July 2025 joint enforcement action against Wise US, a $4.2 million penalty from five state regulators, cited transaction monitoring data integrity issues directly. Regulators are now examining data quality as a root cause, not just program design.

Migrations are the highest-risk data event in a financial institution’s lifecycle. The standard mistake is migrating first and cleaning after go-live. Post-migration cleanup costs five to ten times more than pre-migration remediation because errors propagate through every system that consumed the dirty data before anyone noticed.

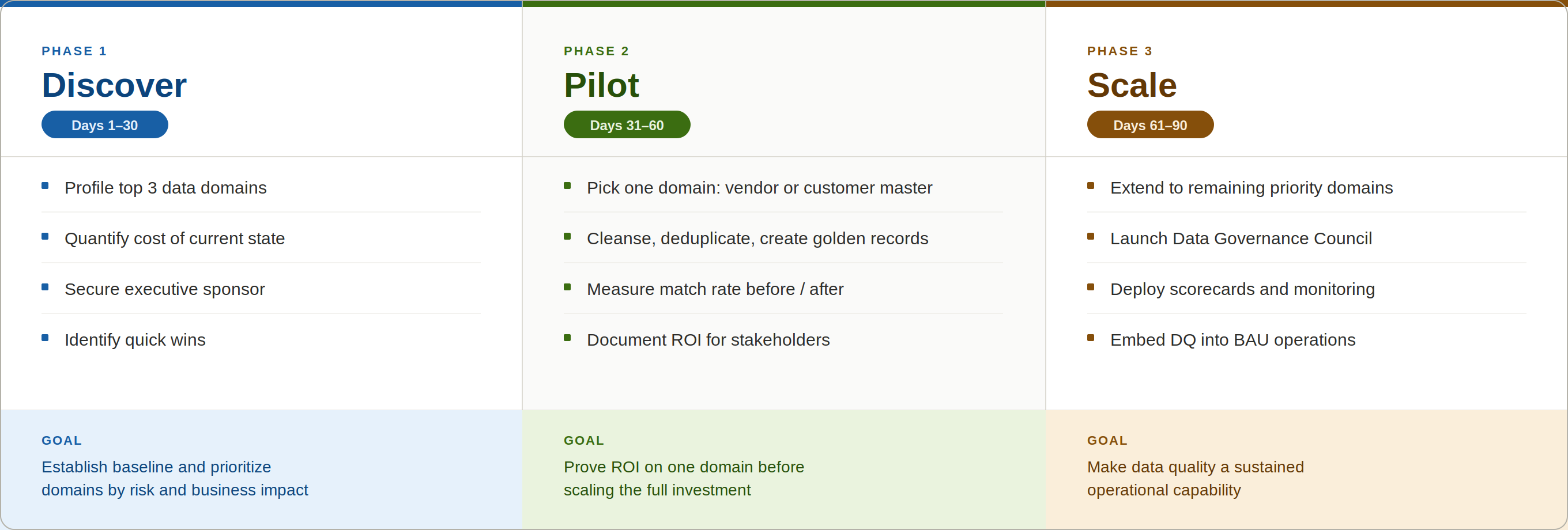

A 90-Day Implementation Roadmap

The 90-day structure below works because it produces proof of value before the program has to justify a full budget commitment. Most data quality initiatives stall not because the technology fails, but because they try to attack every domain simultaneously, with no early win to show leadership.

The phased approach below avoids that trap. The pilot phase is deliberate: one domain, one measurable outcome, one number leadership can point to. By Day 60, you have a before/after match rate, a documented ROI figure, and the organizational credibility to scale.

The most common mistake is starting Phase 2 without a defined success metric. If you cannot answer “how will we know this pilot worked?” before it begins, the output will be interesting observations instead of a business case. Tie the metric to something leadership already tracks: days shaved off the close, duplicate payments prevented, or exceptions cleared per analyst per week.

Five Pitfalls That Sink Most Programs

Treating it as a one-time cleanup. Data quality deteriorates continuously. A cleansing project with no monitoring layer starts decaying the moment it closes.

Single-team ownership. IT-only programs encode business rules incorrectly. Finance-only programs review exceptions but cannot fix them. You need both.

Buying tools before defining rules. A platform configured against undefined rules produces meaningless scores. Agree on what good data looks like in each domain before evaluating vendors.

Ignoring reference and hierarchy data. When a currency code list or cost center hierarchy updates in one system but not others, silent errors propagate into every downstream report that uses those fields.

Failing to connect outcomes to financial metrics. A program that reports DQ scores without translating them into days-to-close improvement or write-offs avoided will not survive a budget review.

Financial data quality management is not an IT project or a finance project. It is a joint operating discipline with defined ownership, measurable outcomes, and a clear path from profiling to production monitoring. The regulatory environment has removed any ambiguity about whether this is optional. BCBS 239 enforcement is escalating. AML fines rose 417% year-over-year in H1 2025. Capital surcharges for data governance failures are documented outcomes, not theoretical warnings.

The institutions that treat data quality as a continuous operating function are the ones that close faster, remediate less, and face fewer regulatory escalations. The 90-day roadmap is a starting point. The end state is a program that runs without requiring a crisis to justify its budget.